Q4 2024 U.S. multifamily market overview

Multifamily demand remained strong through the fourth quarter of 2024, driving absorption rates to levels comparable to the all-time highs of 2021. Meanwhile, rents in major markets are rising again while the Sunbelt is continuing to see strong absorption levels after experiencing a surge in new development. Capital markets activity picked up in 2024, with 2024 sales volumes increasing by almost 10% since the fourth quarter of 2023.

+72.9%

increase in multifamily absorption between 2023 and 2024

31.8%

drop in construction activity over the last 12 months

62.1%

of major multifamily markets had absorption as % of inventory increase by 3% in 2024

34.7%

of total sales activity has been allocated for multifamily assets, outpacing all other product types, including industrial by almost 20%

For more information, contact:

- U.S. Multifamily & Client Data Solutions Lead

- Research

Subscribe to receive national multifamily market reports and insights

Snackable multifamily market insights

-

Nashville investment activity across most sectors began to rebound in 2024

Nashville investment activity across most sectors began to rebound in 2024 -

The Los Angeles multifamily sales market shows gradual recovery amid federal interest rate cuts

The Los Angeles multifamily sales market shows gradual recovery amid federal interest rate cuts -

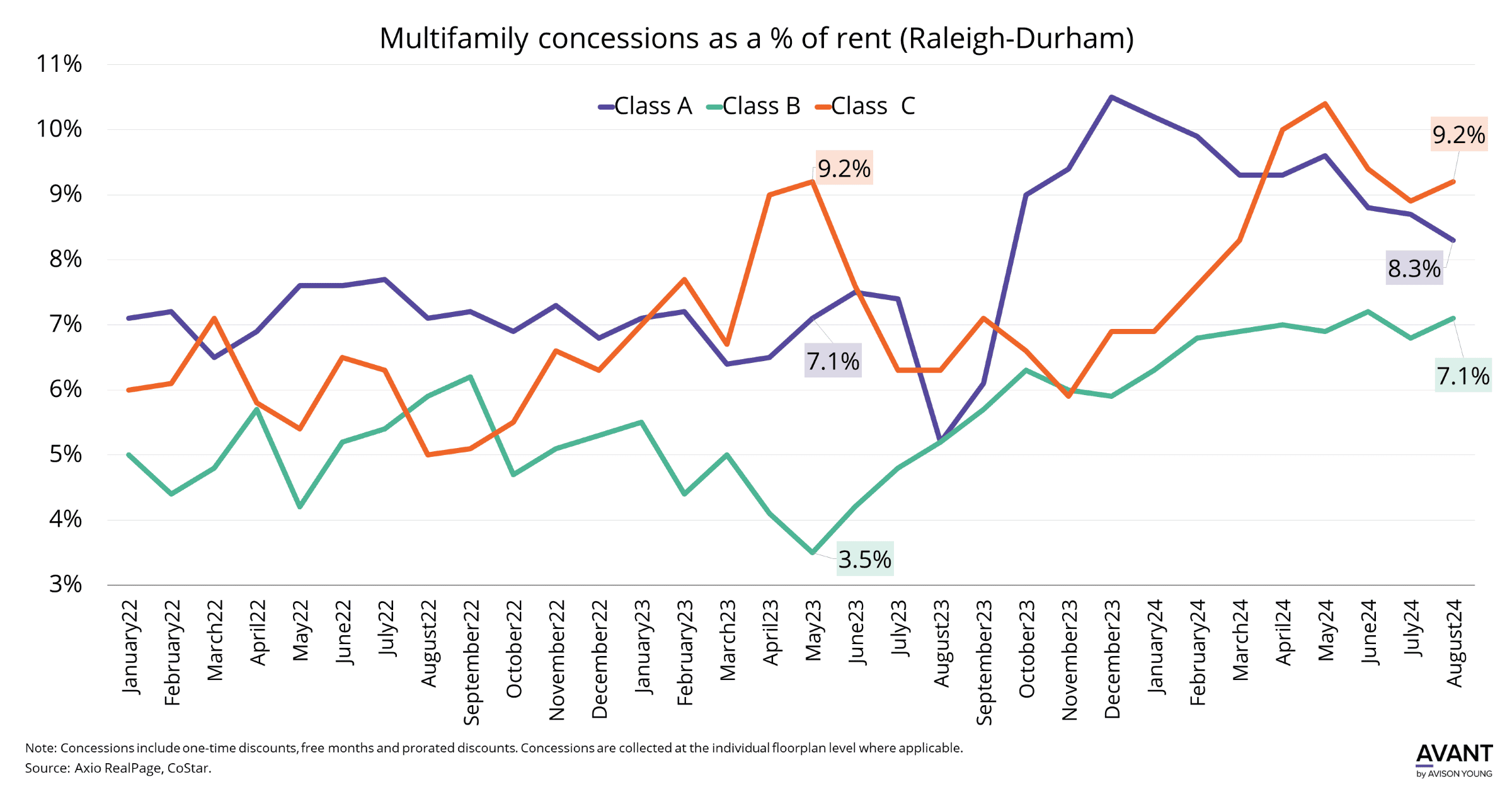

Raleigh-Durham multifamily sees hefty concession growth in classes B and C

Raleigh-Durham multifamily sees hefty concession growth in classes B and C -

Development activity picks up among for-sale housing market across the U.S. while demand increases in multifamily

Development activity picks up among for-sale housing market across the U.S. while demand increases in multifamily