Q3 2024 U.S. industrial market report

The three quarters of 2024 continued to show softness in overall leasing—over 16.5% under the pre-Covid 10-year average—as many occupiers paused decision making due to financial, economic, and political uncertainty before the U.S. election. With the election now finished, and a thin one-party control of the presidency and Congress, we expect an uptick in decision making beginning in the first two quarters of 2025. Deferred decision-making points to probable positive momentum as the historic number of deliveries peaked two quarters ago and continues to decline, and the current construction pipeline drops rapidly to rates not observed since the aftermath of the Global Financial Crisis. The increases in overall vacancy and availability rates nationally have begun to plateau, signaling the approach of equilibrium between supply and demand nationally. Although negative data points and narratives may raise concerns about the strength of the market, several indicators suggest a more optimistic look. A near-historic surge in port activity, record-high U.S. manufacturing construction spending, strong pre-leasing engagement, imminent lease expirations from the pre-Covid and early Covid eras, and slowing new supply introduction collectively signal the market may be stronger than lagging data metrics imply, reflecting conditions from 12 months ago rather than the current situation. Market rental rate growth has plateaued but is steady, albeit stunted in terms of the Covid-cycle increases, with an expected new space gap set to occur at the middle of 2025. The three-day strike and limited disruptions with East and Gulf Coast port workers—whose contract expired September 30 at the heart of holiday preparation season for supply chains—has been quelled with a tentative agreement until January 15. Preparation for this is caused an influx of activity within the ports, positively impacting industrial demand, but is likely to decline heading into the new year. Pent-up and historic levels of dry powder, poised for deployment into industrial assets via acquisitions and development, remains on the sidelines as investors await further interest rate cuts and a policy shift by the Federal Reserve. This significant demand is anticipated to trigger a surge in competition as market players seek to make up for lost time and missed transaction activity.

346.6 msf

First three quarters gross absorption—down 16.5% from the 2010-2019 historical average

Financial, economic, and political uncertainty assisted with users pausing location decision making, at least until there is more certainty after the U.S. election and its potential effects on trade policy.

8.3%

Vacancy is up 420 bps from the low point in the cycle of 4.1% in 2022

The third quarter uptick in vacancy represented the smallest amount since the Federal Reserve began raising rates, signaling supply and demand are close to reaching equilibrium as new deliveries have rapidly stalled.

16%

Current e-commerce percentage of total U.S. retail sales

This marks the first time since the initial surge of Covid online orders that the percentage of e-commerce sales exceeds 16%, a 37.7% jump since the start of 2020.

917,850

Total new EV sales in 2024—an all-time high through the first three quarters of a year

Despite challenging financing conditions for consumers which drastically effected first quarter sales, overall EV sales have surged to all-time highs. EV and its battery production supply chain are emerging as large brand-new sources of industrial demand and will prove to be vital future demand drivers in many markets in the Midwest and Southeast.

$2.1T

Amount of total U.S. construction spending on manufacturing through first three quarters of 2024

Surging from $78.8B to start 2020, U.S. Manufacturing construction spending continues to benefit from reshoring and near-shoring efforts that have been in progress since before Covid. As these projects complete, additional complimentary Industrial demand is expected to rapidly drive absorption across the U.S.

For more information, contact:

-

Director, Industrial / Supply Chain & Logistics Market Intelligence

-

Industrial, Market Intelligence, Strategic Business Advisory

-

Manager, Market Intelligence

-

Industrial, Logistics, Market Intelligence

Subscribe to receive national industrial market reports and insights

Local industrial market reports

Get industrial market trends, data and insights for your commercial real estate market.

- Atlanta

- Boston

- Charleston

- Charlotte NC

- Chicago

- Columbus OH

- Dallas

- Denver

- Detroit

- Fort Lauderdale

- Greenville

- Houston

- Indianapolis

- Inland Empire

- Jacksonville

- Las Vegas

- Los Angeles

- Memphis

- Miami

- Minneapolis

- Nashville

- New Jersey

- Oakland

- Orange County

- Orlando

- Philadelphia

- Phoenix

- Raleigh-Durham

- Sacramento

- San Jose Silicon Valley

- Tampa

- West Palm Beach

Snackable insights

-

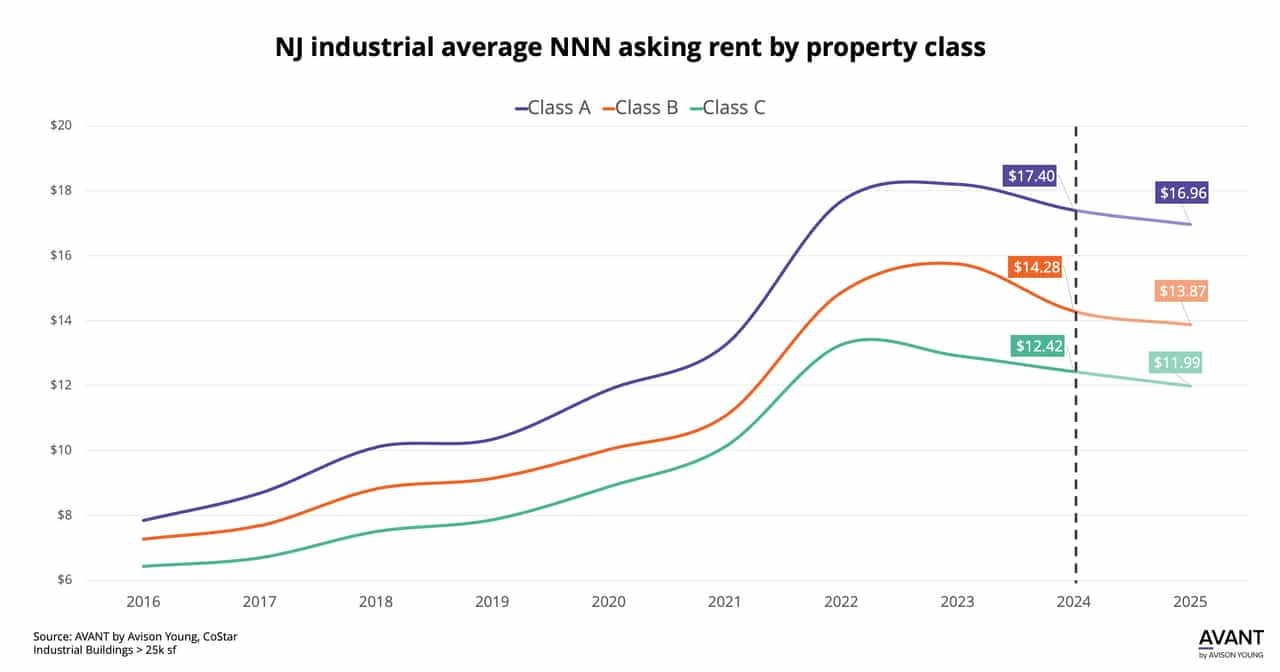

New Jersey industrial average asking rents have dropped by 6.7% YTD

New Jersey industrial average asking rents have dropped by 6.7% YTD -

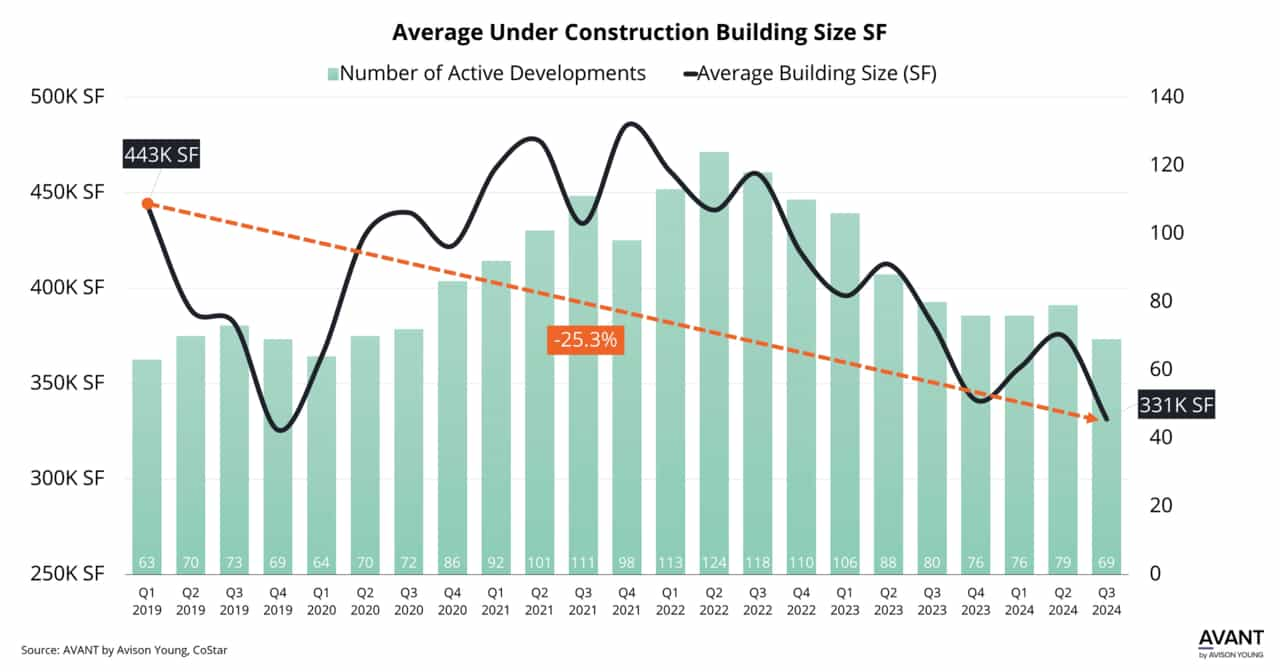

Average under construction building size has fallen 25.3% over the past five years across the Philadelphia industrial market

Average under construction building size has fallen 25.3% over the past five years across the Philadelphia industrial market -

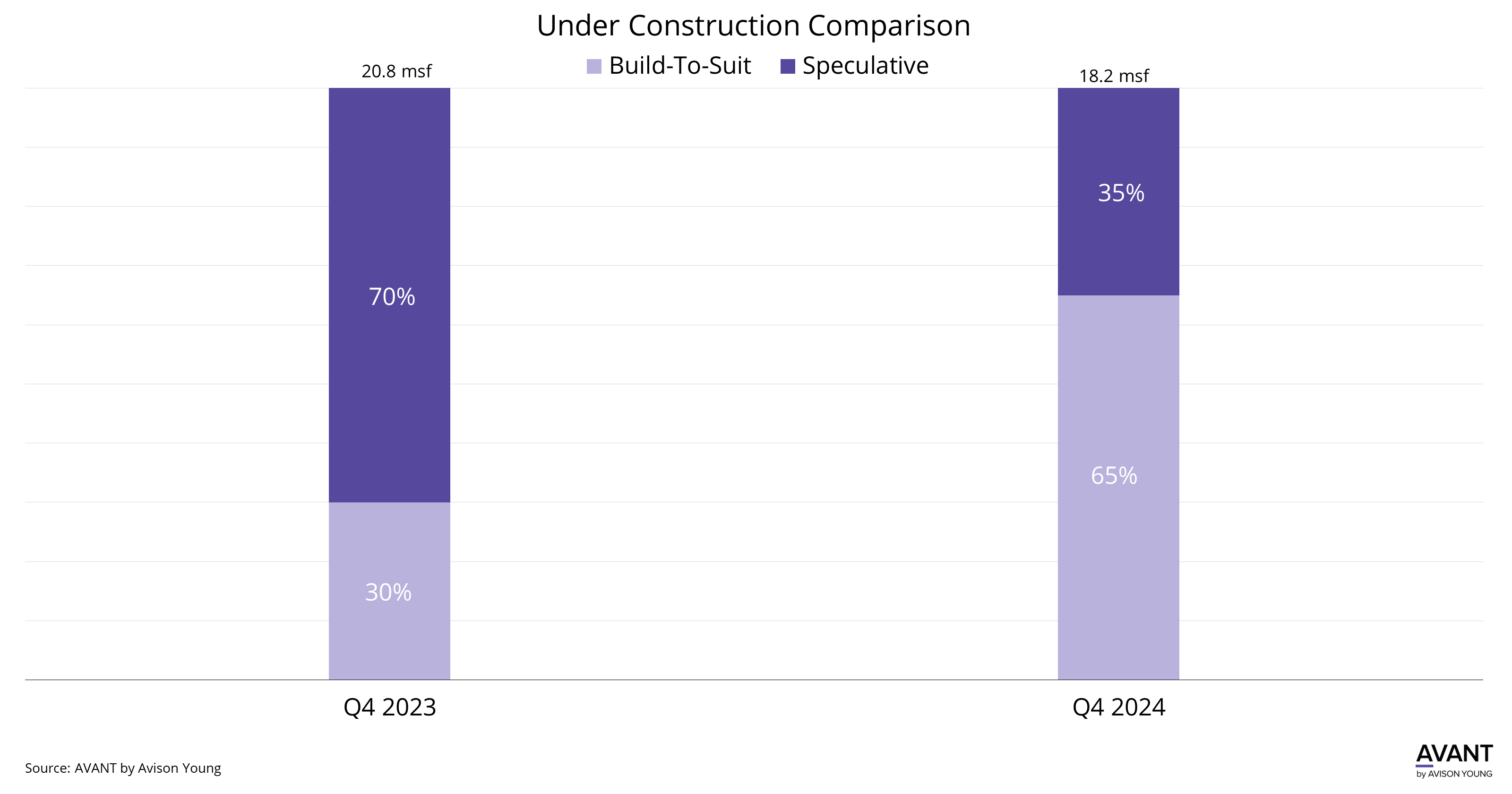

From speculative to secured: the rise of build-to-suit projects in Chicago's industrial sector

From speculative to secured: the rise of build-to-suit projects in Chicago's industrial sector -

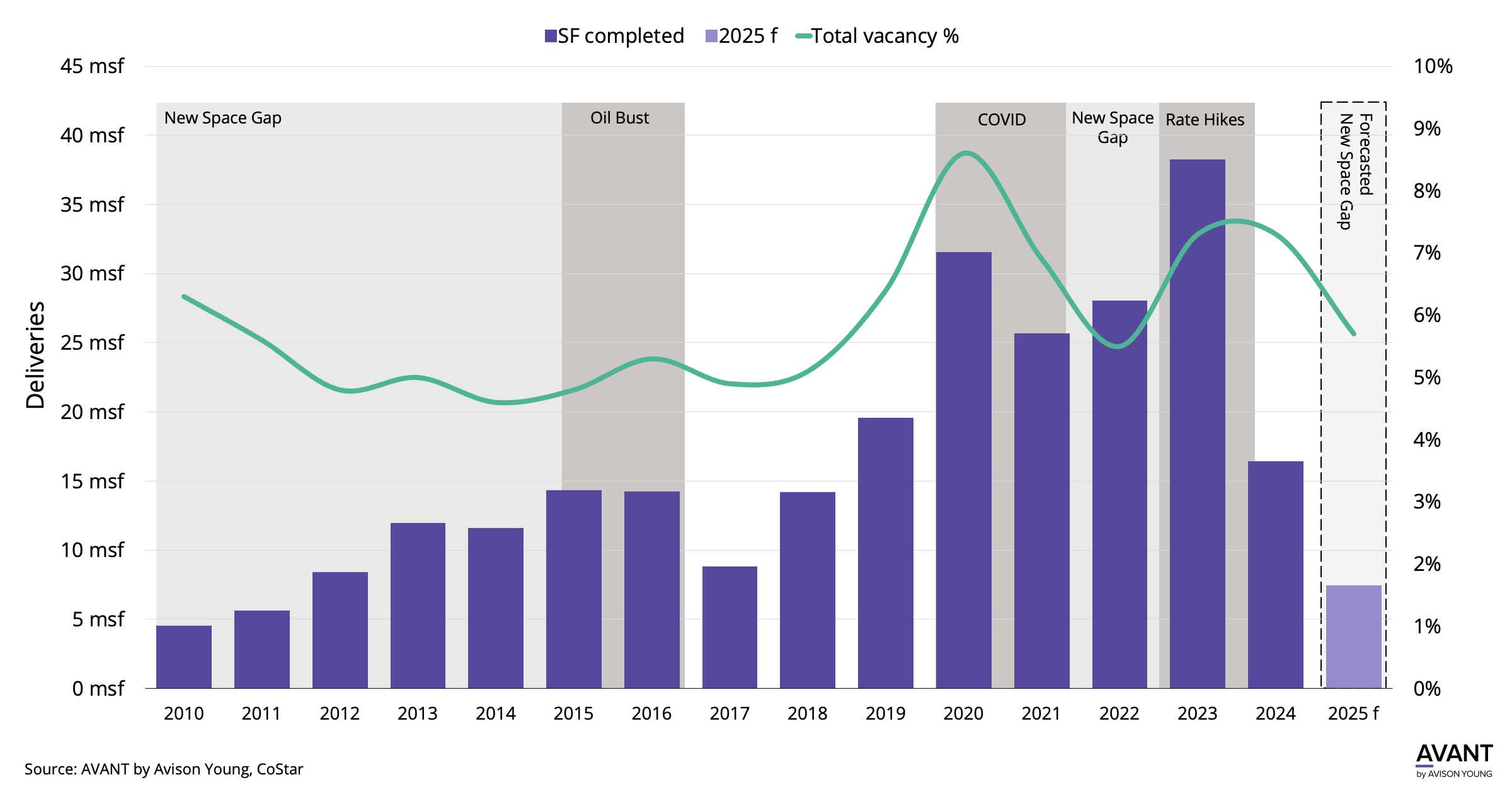

Houston’s industrial delivery space gap is expected to drive down vacancy rates in 2025

Houston’s industrial delivery space gap is expected to drive down vacancy rates in 2025