Q4 2024 U.S. office market overview

The overall availability rate for U.S. office space stood at 23.4% at the close of the fourth quarter, marking the second consecutive quarterly decline in availability—a trend not seen since before the pandemic in Q4 2019. In 2024, U.S. office leasing activity totaled 290 million square feet (msf), falling 11.6% below the pre-COVID annual average of 328 msf (2000–2019) and 1.5% below the 294 msf recorded in 2023. Renewal lease sizes increased by 11.7% since 2019, although this growth has been inconsistent year over year, with the bulk of the increase occurring in 2024.

23.4%

overall availability rate sees second consecutive decrease

The overall availability rate for U.S. office space sat at 23.4% at the end of the fourth quarter—comprised of a 20% direct availability rate and 3.4% sublet availability rate. This quarter marks the second consecutive quarterly decline in overall availability, a trend not seen since before the pandemic in the fourth quarter of 2019.

Year-over-year availability dropped roughly 20 basis points (bps).

Quarter over quarter, direct available space decreased by 9.6 million square feet (msf) and sublet available space decreased by 7.8 msf—netting a 17.3 msf decrease in total available space. While the availability rate remained historically high, this quarterly decrease in supply is a positive indicator for the U.S. office market.

Year-over-year availability dropped roughly 20 basis points (bps).

Quarter over quarter, direct available space decreased by 9.6 million square feet (msf) and sublet available space decreased by 7.8 msf—netting a 17.3 msf decrease in total available space. While the availability rate remained historically high, this quarterly decrease in supply is a positive indicator for the U.S. office market.

290 msf

U.S. office leasing activity in 2024

U.S. office leasing activity in 2024 reached 290 msf—sitting 11.6% behind the pre-COVID average (2000-2019) at 328 msf, and 1.5% behind 2023 at 294 msf.

However, certain markets like San Francisco, Manhattan, and Dallas are up significantly from 2023 (50%, 18%, and 11%, respectively). Additionally, the Federal Reserve’s recent interest rate cut should continue to provide a boost in the office market in the coming quarters.

However, certain markets like San Francisco, Manhattan, and Dallas are up significantly from 2023 (50%, 18%, and 11%, respectively). Additionally, the Federal Reserve’s recent interest rate cut should continue to provide a boost in the office market in the coming quarters.

11.7%

increase in average renewal square footage vs. 2019

Since 2019, average lease sizes across the U.S. have steadily declined, with 2024 marking a 14.7% decrease compared to 2019. This trend is primarily driven by new leases, which have shrunk by 18.6% as occupiers transition to more efficient office spaces.

In contrast, renewal lease sizes have grown by 11.7% during the same period, though this growth has been inconsistent year over year, with the majority occurring in 2024. This uptick in renewal sizes highlights large occupiers leveraging current market conditions to secure larger spaces through renewals, hinting that the market is soon to hit recovery mode.

In contrast, renewal lease sizes have grown by 11.7% during the same period, though this growth has been inconsistent year over year, with the majority occurring in 2024. This uptick in renewal sizes highlights large occupiers leveraging current market conditions to secure larger spaces through renewals, hinting that the market is soon to hit recovery mode.

For more information, contact:

- Senior Manager, U.S. Office Lead, Market Intelligence

- Market Intelligence

Subscribe to receive national office market reports and insights

The Office Busyness Index

The analytics behind building utilization

Busy places can create vibrant, lively and enriched experiences. Build connectivity and spark energy. And, fuel financial performance.

Snackable office market insights

-

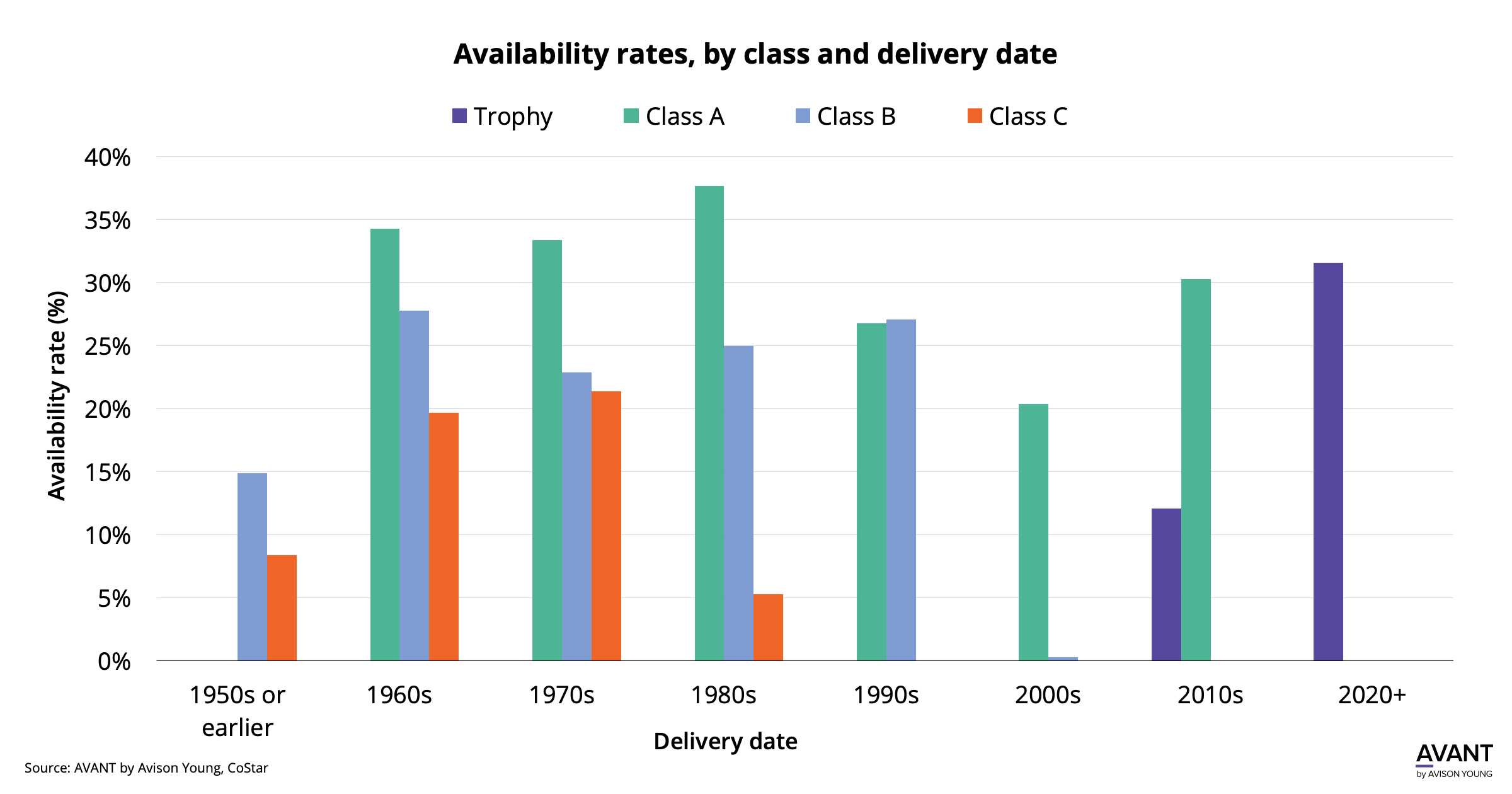

Office availability rises as Nashville tenants seek upgrades

Office availability rises as Nashville tenants seek upgrades -

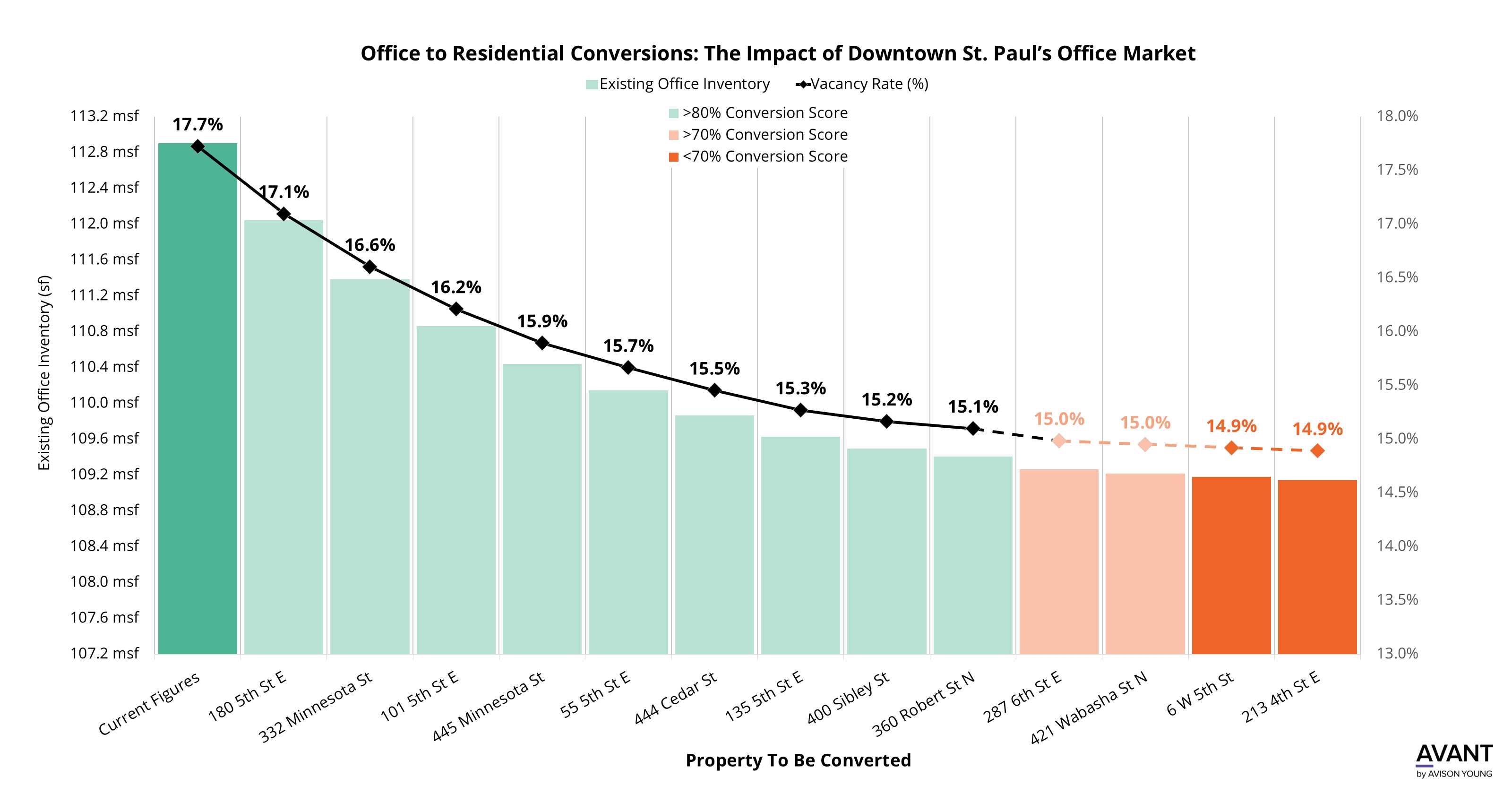

MSP’s office market could see 260 bps reduction in vacancy following office to residential conversions identified in St. Paul’s downtown

MSP’s office market could see 260 bps reduction in vacancy following office to residential conversions identified in St. Paul’s downtown -

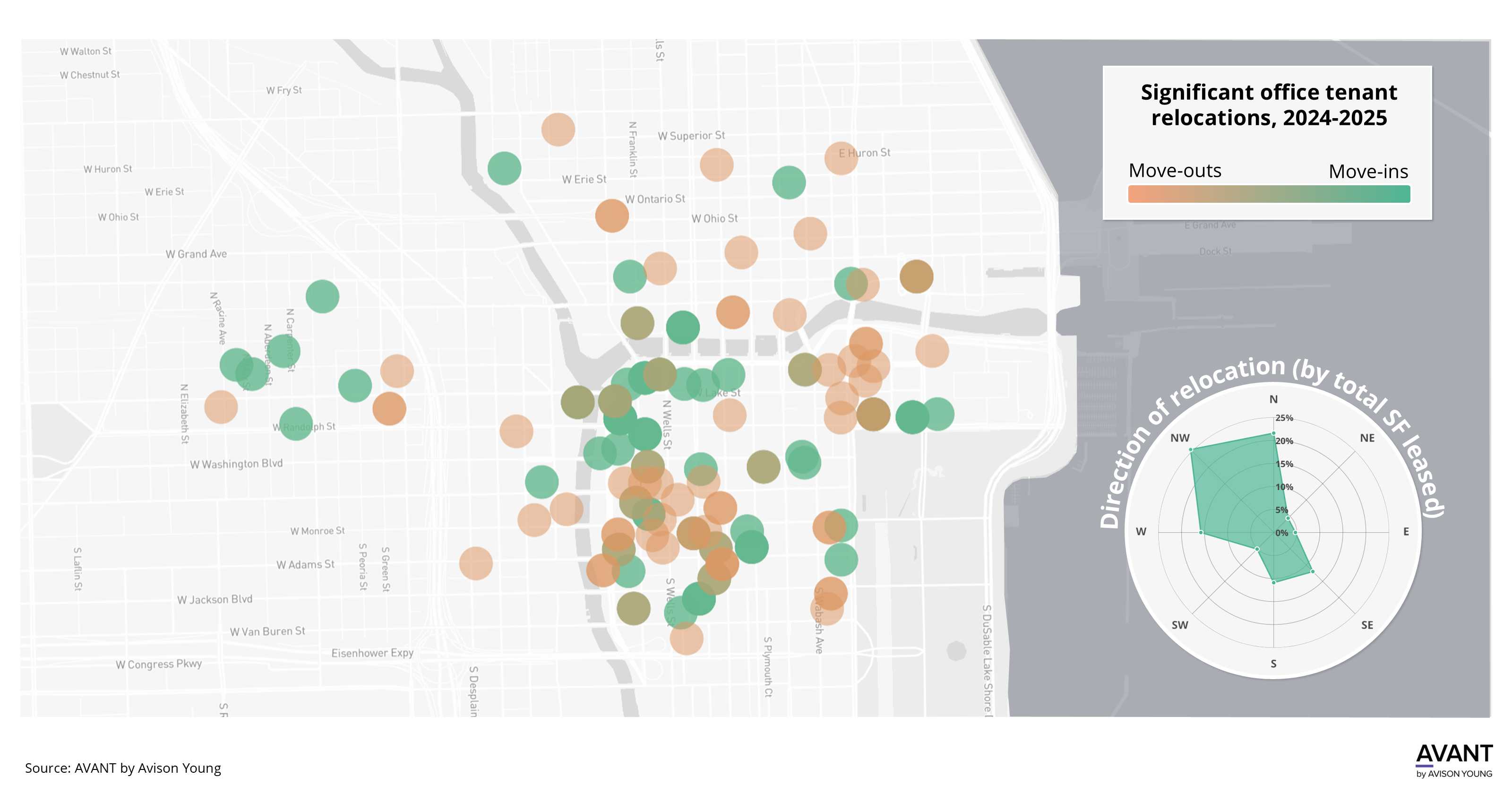

Shifting migrations: northwest movement of office tenants in the CBD

Shifting migrations: northwest movement of office tenants in the CBD -

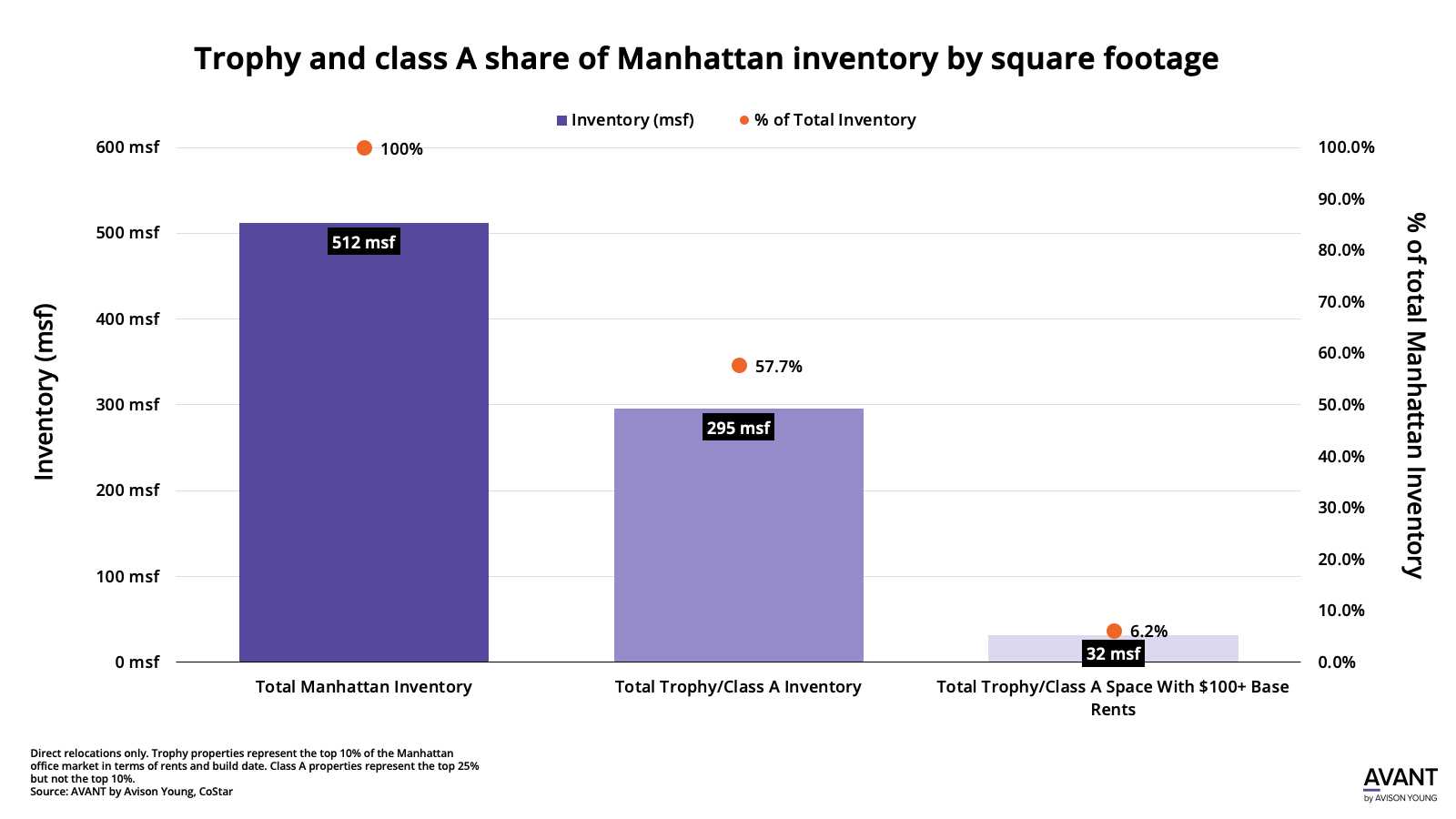

6.2% of Manhattan inventory commanded triple-digit base rents in 2024

6.2% of Manhattan inventory commanded triple-digit base rents in 2024

Local office market reports

Get office market trends, data and insights for your commercial real estate market.

- Atlanta

- Austin

- Boston

- Charleston

- Charlotte NC

- Chicago (Downtown)

- Chicago (Suburban)

- Dallas

- Denver

- Detroit

- Fairfield-Westchester

- Fort Lauderdale

- Greenville

- Houston

- Indianapolis

- Jacksonville

- Las Vegas

- Long Island

- Los Angeles

- Miami

- Minneapolis

- Nashville

- New Jersey

- Manhattan

- Oakland

- Orange County

- Orlando

- Philadelphia

- Phoenix

- Pittsburgh

- Raleigh-Durham

- Sacramento

- San Francisco

- San Jose Silicon Valley

- San Mateo

- Tampa

- Washington DC (Northern Virginia)

- Washington DC (Downtown)

- Washington DC (Suburban Maryland)

- West Palm Beach